© Europa.eu

Going up in the world takes effort and earns you few friends. Every President of the European Central Bank has come in for criticism, probably because every financial journalist in the world, as well as every politician with some financial nous, thinks they could do it better. This is almost certainly not the case; it may be a job in which it is quite impossible to please everybody. Remember the urbane and charming Wim Duisenberg, the ECB’s first leader? I was there in order to interview him when he first assumed this high – and unprecedented – office in June 1998, while my cameraman got shots of him sitting at his new desk.

He was succeeded in 2003 by Jean-Claude Trichet, who always stopped for a chat with me whenever he visited the European Parliament in Strasbourg and happened to pass my camera position near the entrance to the Chamber. I liked him, but then, I’m not an economist. A former General Director of the Treasury at France’s Ministry of Finance and also a former governor of the Bank of France, Trichet’s term included the European Sovereign Debt crisis, and he was criticised at the time by French President Nicolas Sarkozy for not pursuing a more growth-orientated policy during his seven years in charge. However, he kept interest rates under control and is credited with recording a better performance at the time than Germany’s Bundesbank managed.

Next, in 2011, came Mario Draghi, a widely experienced but perhaps more sombre figure but clearly in control and running the institution his own way. He famously said that he would be prepared to do “whatever it takes to prevent the euro from failing”. Indeed, he is widely credited with having saved the currency during the European debt crisis, earning him the media nickname “Super Mario”. So Super, in fact, that he was invited by Italian President, Sergio Mattarella, to former a ‘government of national unity, which he has headed as Prime Minister since February 2021 And that brings us to the fourth and present incumbent at the ECB: Christine Lagarde, the subject of this article.

She has certainly attracted criticism since she took office in November 2019. Perhaps most recently, it was the popular German newspaper Bild that accused her of destroying people’s earnings as well as their savings by permitting inflation to rise. Bild had said much the same in 2019 in criticism of Lagarde’s predecessor, Draghi, so it will come as no surprise. It was very critical of Draghi getting the job instead of its preferred (German) candidate, suggesting that Italians were profligate and would cause chaos. Draghi did not, of course, and we can put this down as an example of Bild’s nationalism. The German public, like the peoples of other countries, are hostile towards the idea of inflation eroding the value of their money. It’s been reported that quite a lot of Germans think the ECB is a bit too loose with its controls, which means that their anguished cries are bound to be picked up and echoed by a popular newspaper. Bild described Lagarde as “Madame Inflation” (which makes her sound more like a balloon than an economist). This latest attack came shortly after the ECB’s decision not to take counter measures when consumer prices hit a 13-year high. Lagarde is, it seems, unmoved.

“The current increase in inflation is expected to be largely temporary and underlying price pressures are building up only slowly,” she told a press conference at the ECB’s splendid Frankfurt headquarters. “The inflation outlook in our new staff projections has been revised slightly upwards, but in the medium-term inflation is foreseen to remain well below our two per cent target.” She told journalists that inflation is expected to rise further towards the end of this year before coming down again in 2022.

In a speech she gave in Lisbon in early November, Lagarde compared the Covid crisis with the massive earthquake that rocked the city one early November morning in 1755, costing up to 30,000 lives and also up to 48% of Portugal’s GDP at the time. It was a terrible tragedy, but from it changes were made that benefited the people of Portugal over the years ahead. “We have also faced a human tragedy, with over 800,000 people in the EU losing their lives,” she told her audience, referring to the pandemic. “We have reacted decisively to prevent even worse outcomes: policies have worked together in an unprecedented way to preserve jobs and stave off bankruptcies. And now we have a chance to transform the economy, accelerating the necessary green and digital transitions and protecting ourselves in a fast-changing world.” Reform will certainly be needed: the pandemic has caused the euro area’s biggest GDP fall on record. Lagarde then went on to explain how the bank had reacted and how that had helped. “Our pandemic emergency purchase programme (PEPP) ensured that financing conditions for all sectors of the economy remained favourable,” she reminded her audience, “even during the darkest moments of the crisis. Coupled with measures taken by ECB Banking Supervision, our policy response is estimated to have saved more than one million jobs.” The monetary Policy Decision of 21 October reiterated the determination that there exists no current reason to raise interest rates, “The Governing Council continues to judge that favourable financing conditions can be maintained with a moderately lower pace of net asset purchases under the PEPP than in the second and third quarters of this year,” it said in a press release.

TALES FROM THE CRYPT (-ocurrency)

Lagarde is not likely to be popular among those who invest and trade in cryptocurrencies, of which there are now a growing number. She told an audience at the European University Institute that Crypto-currencies are only useful for money laundering.

In an interview on the David Rubenstein show on Bloomberg and other channels, Lagarde said she believes the word “cryptocurrency” is a misnomer. “Cryptos are not currencies, full stop,” she declared. “Cryptos are highly-speculative assets that claim their fame as currencies, but they are not. I think we have to distinguish between cryptos that are highly speculative, suspicious occasionally, and high intensity in terms of energy usage. Assets, but not a currency.” There are those boldly claiming to have made a fortune dealing in crypto currencies without having any knowledge of finance or the markets. Some of these tales are clearly a form of advertising and should only be heeded by those who are really competent and knowledgeable about such things. However, it’s clear that whatever Lagarde may have said in the past, the idea of an ECB-backed cryptocurrency hasn’t gone away.

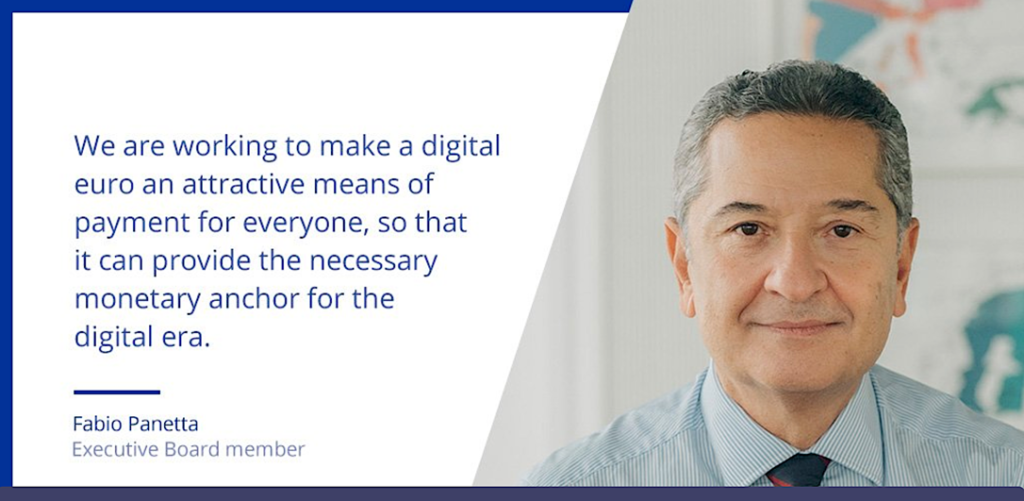

In October 2021, she replied to a written query from German MEP Gunnar Beck, suggesting that the idea is still under consideration. “As regards so called ‘crypto-currencies’ which you refer to in your letter, let me point out that they are not without risk and are not fit to serve Europeans as an alternative to the euro, as official currency, in terms of basic monetary functions (a store of value, a means of payment, and a unit of account).” So don’t expect to switch to crypto-euros any time soon. However, she goes on to say: “A digital euro would be very different from crypto-assets: people using it could have the same level of confidence as with cash, since like cash, a digital euro would also be backed by a central bank.” Lagarde reminds Beck that the ECB’s Governing Council decided on 14 July to launch “the investigation phase of a digital euro project,” adding that “The launch of this phase does not anticipate any future decision on the possible issuance of a digital euro.” Research by Eurobarometer suggests that the public have great faith in the euro as a currency, with 79% of correspondents backing the single currency.

Meanwhile, investigations into where to take it next continue, in the awareness that the use of credit cards continues to grow in every member state while the use of notes and coins for day-to-day transactions declines. Our world is becoming more and more digital, whether we like it or not. Research continues with the European Parliament about the legal instruments that would be needed as well as with the European Commission on how the digital euro would work. This research phase is scheduled to last for twenty-four months. “A digital euro,” says the Bank, “must be able to meet the needs of Europeans while at the same time helping to prevent illicit activities and avoiding any undesirable impact on financial stability and monetary policy.” Apart from the European Parliament and other European decision-makers, citizens, merchants, and the payments industry will also be involved, according to ECB Board Member Fabio Panetta, Chair of the High-Level Task Force on a digital euro.

There is controversy over cryptocurrencies, however, quite apart from their seemingly unavoidable volatility, and much of that stems from widespread ignorance of exactly what they are and how they work. Even experts agree that the technical controls and source codes that support and secure cryptocurrencies are extremely complex. The value of a transaction is still expressed traditionally, so if we call our fictional cryptocurrency splat, then you can talk about 3.5 splats, just as you would talk about 3.5 euros, dollars, or roubles, for instance. Cryptocurrencies rely on something called a blockchain, which is the master ledger, storing all the previous activities and transactions. The blockchain validates the ownership of every unit of the currency at any given time. Identical copies of the block chain are stored in every node of the software network for the cryptocurrency. Unless you’re a tech-minded individual who can read the stock market figures (just the figures, not the text) without getting bored, this is where it all gets difficult. The blockchain is a network of decentralized server ‘farms’, as they’re called, that are run by computer-savvy individuals or groups of individuals known as ‘miners’. These people record and authenticate cryptocurrency transactions all the time, without pause. No transaction is considered finalised until it has been added to the blockchain, at which point, unlike a credit card transaction, it is irreversible. This has been one aspect of the whole thing that has put potential users off, so some of the newer cryptocurrencies have been developing ways to overcome this drawback. Holders of cryptocurrencies have a ‘key’ that can be up to 78 digits long, which they must retain. Lose it and you have lost your money; it cannot be recovered.

The aim of most of the supporters of cryptocurrencies is to create a decentralised finance system, known as ‘Defi’, which sounds almost laudable: a financial system not under the control of the normal regulators and therefore more open to innovation. It’s also referred to as the ‘metaverse’. The Economist magazine described it as similar to going down the rabbit hole, as Alice in Wonderland did in Lewis Carroll’s famous books. The traveller enters an unreal place where they are represented by avatars of their choice. “The ultimate goal,” says The Economist, “is to replace intermediaries like global banks and tech platforms with software built on top of networks so that the value they generate goes back to the users who own and run them.” The article points out that it could all lead to a “better type of finance: a system that is quicker, cheaper, more transparent and less reliant on powerful centralised institutions.” This is, however, to ignore the fact that these powerful centralised institutions can be sued if things go horribly wrong. Who does one sue in a Defi?

To buy cryptocurrencies, should you wish to, you have to go on-line to one of the several brokers dealing in them. You must then tell them how much you want to invest and in which cryptocurrency. The dealer sites most often recommended (but I’ve never visited their sites, so what do I know?) are Etoro, Libertex and Crypto Rocket, but there are many more with reasonable star ratings. Top Brokers Trade website warns that even the virtual ‘wallets’ used by cryptocurrency holders can be vulnerable to electronic theft. Since the ‘miners’ clearly don’t do any real digging, nor lift a tool heavier than a pencil, what do they do? Top Traders explained it like this: “Cryptocurrency miners serve as record-keepers for cryptocurrency communities, as well as indirect arbiters of the value of the currencies.” With the use of vast amounts of computing power, often manifested in server farms that are privately owned by mining collectives that comprise of dozens of individuals, the miners use methods that are highly technical to verify the completeness, accuracy, and security of currencies’ block chains. “The scope of the operation isn’t much different to the search for new prime numbers, which also requires massive amounts of computing power,” the website points out. The new Mayor-elect of New York, Eric Adams, has nevertheless said he’ll take his first three months’ pay in bitcoin and turn his city into the “centre of the cryptocurrency industry”, where more server farms can be established.

It seems that the Mayor of Miami, Francis Suarez, may have influenced the decision with an email sent to Adams when his victory was announced. Suarez has said he will also take his next paycheque in bitcoin.

Bitcoin, the first and best-known cryptocurrency, is reported to use 121 Terrawatt-hours every year to verify and guarantee transactions. That’s more electricity than Argentina uses, while etherium consumes as much power as Qatar. Environmentalists are worried because the ‘mining’ operation becomes less and less efficient as the value of a cryptocurrency goes up, which means that the more it is used the more energy will have to be generated to power the computers running the transactions. According to a report by CNBC, bitcoin mining accounts for about 35.95 million tons of carbon dioxide emissions each year—about the same amount as New Zealand. Defenders of cryptocurrencies argue that much of the power they use comes from renewable sources, but quite a lot doesn’t. Environmentalists fear that cryptocurrencies will continually increase the demand for energy beyond the point where it is sustainable. The already fairly empty promises of the COP26 meeting in Glasgow will become emptier still.

OUT AND ABOUT

What about the ECB and the wider world? Certainly, the wider world watches what the Bank is doing and listens to what Lagarde has to say, even if it sometimes doubts what she has said. Take the case of interest rate rises, for instance. She has told a number of meetings recently that the ECB is unlikely to raise interest rates in 2022, although some forecasters expect that to happen by next October. Despite what she said, inflation is currently running at a 13 -year high and the markets have been betting that the ECB’s policy will come under a lot of pressure and may force an about-turn in policy for the first time in more than a decade. Lagarde doesn’t see it that way. “In our forward guidance on interest rates, we have clearly articulated the three conditions that need to be satisfied before rates will start to rise,” she told an event in Lisbon, going on to add that despite the current inflation surge, the outlook for inflation over the medium term remains subdued. Any rise in inflation is thought by the ECB to be transitory.

Lagarde, though, is not blind to the risks and pitfalls lying ahead for Europe. She warned that the globalized nature of the euro area’s economy makes it highly vulnerable to systemic shocks from supply chain disruptions. “There are signs that the global economy could increasingly be a source of shocks for Europe rather than a stabilizer against volatility,” she said. What about Russia, with an upcoming election and its sights still set on Kyiv? It’s not clear if Lagarde has changed the view she held in September 2017as President of the International Monetary Fund (IMF), when she said: “Russia is not interested in the economic collapse of Ukraine.”

She may feel reassured but people I know in Kyiv are not. According to Lagarde, she hopes that Russian support for Ukraine’s economy will continue. However, there is virtually no prospect of access to any financial facilities being extended to Moscow. Russia remains subject to economic sanctions first imposed in 2014 in response to Russian actions in Ukraine. Ukraine itself, on the other hand, is seen as a ‘priority partner’ for the EU, which remains Ukraine’s main trading partner, representing 42% of Ukraine’s total trade, and with a fairly balanced split between imports and exports. Ukraine has recently passed a draft law to legalize cryptocurrencies with a view to opening up the crypto market to businesses and investors by next year. Even so, Lagarde seldom makes public comments on what is happening in Ukraine, nor in Belarus, but that doesn’t mean changes don’t occur. In February 2021, the Board of the National Bank of the Republic of Belarus approved an instruction on safe and developmental banks, including the European Central Banks, so the door is opening for dialogue and even, perhaps, for possible transactions.

In 2019, the National Bank of the Republic of Belarus (NBRB) said it was “looking forward to a new twinning project with the European Union”. NBRB Deputy Chairman Sergei Kalechits was speaking at the final conference of the European Union’s twinning project designed to enhance the potential of Belarus’ central bank. According to the Belarus government’s official website, Belarus.by, NBRB Deputy Chair Sergei Kalechits said that the central bank had become the first Belarusian body to implement a twinning project. “We think highly of the results,” he said. “We and our European partners have reached a preliminary agreement on starting work on preparing a new twinning project involving the National Bank.”

In his words, the joint use of the expert potential of Belarus’ central bank and the central banks of European Union countries in the course of the twinning project allowed both sides to secure significant practical results in matters of financial stability, banking oversight, protection of rights of consumers of financial services, the payment system and information technologies, the management of financial risks, and the communication policy.

However, even the calmest of seas (and the current ones are arguably not so much calm as ‘caught between waves’) can contain sharks. One of them could arguably be Vladimir Putin, although Lagarde has clearly had a long affection for Russia. In 2018, when she was still Managing Director of the International Monetary Fund, she gave a talk in St. Petersburg, saying: “It is a great joy to be back in St. Petersburg, which is one of my favourite places. It is hard to top the beauty of the surroundings, the elegance of the architecture, the magnificence of the art, and the warmth of the people.” Nothing ambivalent there, and nothing much to argue with. It is a truly beautiful city and the trams (when I was there) were an extremely cheap way to get about, if somewhat ‘rustic’ to ride in; they have probably been modernised since then. Lagarde went on to say that “challenges are best solved in an ethos of cooperation, by deepening ties among the family of nations, and by heightening collaboration in the service of the global common good.” That won’t be easy, given the EU’s range of sanctions against Russia.

The European Bank for Reconstruction and Development has predicted that the Russian economy will grow by 3.0% in 2022, having already expanded by 4.3% this year, and Russia’s GDP is reassuringly buoyant, it seems. Russia’s statistics agency, Rosstat, has recently raised its estimate for Russian GDP growth for the second quarter of 2021 to 10.5% annualised.

What’s more, Maxim Reshetnikov, head of Russia’s Ministry of Economic Development and Trade, said the potential for further recovery has not yet been exhausted, even if industrial output has not yet reached pre-pandemic levels. Russia has raised its interest rate to 6.75% in a bid to control inflation, and in the ECB’s Governing Council there are quite a number of members not reassured by the eurozone inflation figures who feel a rise in its interest rates would be better sooner, under tight control, than suddenly later as a panic measure. In much of Eastern Europe the rates have already risen.

NAUGHTY, NAUGHTY – OR NOT?

Lagarde herself faced trial in a French court in 2016 and the court found her guilty of negligence for approving an award of €404-million to the controversial businessman Bernard Tapie for the disputed sale of a company. She was still managing director of the IMF at the time, but despite the guilty verdict she was not punished. She denied wrongdoing and was not in court for the hearing. The board of the IMF said afterwards that it retained full confidence in Lagarde, as did the French government who promptly reappointed her to her IMF post.

The actual charge was “negligence by a person in a position of public authority”. It involved the alleged misuse of public funds, not corruption, but it could have carried a sentence of one year in prison and a fine of €15,000. Instead she walked away without even a criminal record. The judge who heard the case, Martine Ract Madoux, said she had taken into account the difficult position in which Lagarde had found herself in the middle of the financial crisis, as well as her ‘good reputation’ and her ‘international standing’.

This was a rare case and it’s worth remembering that the Cour de justice de la République (Court of Justice of the Republic) is made up mainly of politicians, not judges, and it mainly handles allegations of crimes allegedly committed by cabinet ministers. It not the first time the CJR has found an accused person guilty and set them free. Tapie was a majority shareholder in the Adidas sports goods company but when he became a cabinet minister in the government of François Mitterand, he had to sell the company. After his compensation, approved by Lagarde, he was ordered to pay back €404-million plus interest. It came about because in 1993, Tapie sought to sue Credit Lyonnais for allegedly undervaluing the company and thereby defrauding him.

The case was passed to Lagarde who was Finance Minister under Nicolas Sarkozy, a conservative president, and compensation was duly paid out the following year, much to the annoyance of the public, who saw the compensation as ‘public money’ being paid to an extremely wealthy man, Credit Lyonnais being state-owned. Tapie was eventually obliged to pay back the money with interest.

The pay-out had clearly been Lagarde’s fault, but she was left, as the old British phrase has it, “without a stain on her character”.

The court case is yesterday’s news, however, and Lagarde seems to have moved on successfully, putting it all behind her. The more interesting question for the markets now is how determined is she to resist raising interest rates? The markets don’t seem convinced by her denials and have already priced in a rate increase for some point during 2022, despite the ECB’s promise to keep rates low and predicting that the uptick in inflation is a temporary phenomenon that the Bank expects to go down again in the New Year. The tentative rate increase means that the major debtors, such as Italy, will face higher costs. It prompted Lagarde to promise again that rates would not rise, or at least that such a rise would be “very unlikely”. As a result, the yields on Eurobonds fell. The European Central Bank has made any increase conditional on inflation stabilising at 2%, but the Bank’s experts foresee a gradual fall and economists are predicting that by 2023 inflation could be as low as 1.5%.

The big decisions will come this December: even Lagarde can’t deny rising prices, despite her assurances. Inflation in the eurozone, even if it drops next spring, is currently the highest in more than a decade, with supply shortages slowing down recovery from the pandemic. Some have been predicting a reduction in the Bank’s €1.85-trillion bond purchase programme, se t up to save the eurozone economy during the pandemic. A shortage, for instance, of computer chips is holding up production in the car industry, delaying recovery. A worrying sign is that inflation in the eurozone hit 3.4% in September, and some say it could rise to 4% before the year’s end, but ECB experts say that’s a temporary glitch and that over the medium term it will not get anywhere near the 2% threshold the ECB has set itself. In any case, inflation in the eurozone is less pronounced than it is in the United States, because European governments spent less on feeding stimulus money into the economy. Meanwhile, the ECB’s lending rate to banks stands at 0%, while banks that want to deposit money overnight must pay -0.5%, so the only way for banks to avoid that cost is to use the money to lend at interest to enterprises instead, thus hopefully stimulating the economy.

The pandemic is sadly not over, with some countries still making panicky decisions and not showing much resolve. Lagarde mentioned the problem in her speech in Lisbon. “Externally, the pandemic has shown us how vulnerable we are to disruptions that threaten the global trading order – and this is particularly true for Europe, with our deep integration into the global economy,” she said. “Indeed, today’s supply chain disruptions may only be a dress rehearsal for some of the difficulties we will face when natural disasters become more frequent, or if international relations become more fraught and supply chains start to be influenced by geopolitical biases.” Lacking a crystal ball, Economic forecasters can only make predictions based on facts, figures and trends, so Lagarde is urging Europe to pay attention to the ways things are going in order to build for the future. “On the internal front, we need to step up our investment in the sectors of the future,” she said. “And we have an ideal tool for the job: the €750 billion Next Generation EU (NGEU) fund. It gives us a mechanism to stay focused on future-oriented investment even when national fiscal policies become less expansionary after the pandemic. And it helps reduce the green and digital divide within Europe, which is crucial for ensuring that future growth is equitable.” Lagarde warned, however, that not every eventuality can be predicted. “On the external front, we need to be ready for a more uncertain world. As I have recently argued, this means using Europe’s economic weight to support reciprocated trade openness globally, while strengthening its own domestic demand to insure against a more volatile global economy.”

Lagarde is not without her critics, of course, and some of the German media have descended to raw sexism in their attacks. They have suggested that her apparent affection for high fashion and luxury goods have blinded her to the plight of the poor and the elderly. Leading the attack was Bild, of course. “Lagarde likes to wear luxury fashion including Chanel,” it trumpeted, “earns almost €40,000 a month — but she doesn’t seem to care about the worries of normal people.” Bild even nicknamed her ‘Luxury Lagarde’. As the Politico on-line news source pointed out, the paper also calculated “that surging inflation would cost each German saver €1,400 this year — a sum that Lagarde can only laugh about, it added. For this money she would only get the arm of a Chanel blazer,” it wrote, adding somewhat unfairly that “Some of the ECB president’s luxury jackets cost €7,000 and more.” Whatever the papers say, Lagarde will probably continue to be a fashion ikon, although she would probably prefer to be remembered as the woman who helped save the euro.